The goal of cvwrapr is to make cross-validation (CV)

easy. The main function in the package is kfoldcv. It

performs K-fold CV for a hyperparameter, returning the CV error for a

path of hyperparameter values along with other useful information. The

computeError function allows the user to compute the CV

error for a range of loss functions from a matrix of out-of-fold

predictions. See the package vignettes for more examples.

You can install the development version from GitHub with:

# install.packages("devtools")

devtools::install_github("kjytay/cvwrapr")This is a basic example showing how to perform cross-validation for

the lambda parameter in the lasso (Tibshirani 1996).

# simulate data

set.seed(1)

nobs <- 100; nvars <- 10

x <- matrix(rnorm(nobs * nvars), nrow = nobs)

y <- rowSums(x[, 1:2]) + rnorm(nobs)

library(cvwrapr)

library(glmnet)

set.seed(1)

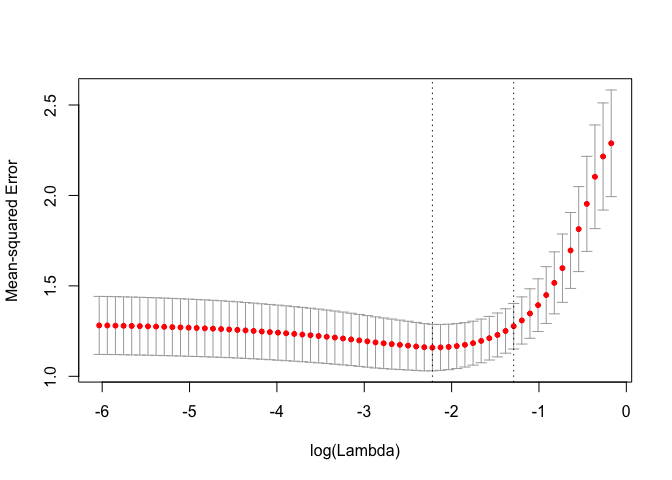

cv_fit <- kfoldcv(x, y, train_fun = glmnet, predict_fun = predict)The returned output contains information on the CV procedure and can be plotted.

names(cv_fit)

#> [1] "lambda" "cvm" "cvsd" "cvup" "cvlo"

#> [6] "lambda.min" "lambda.1se" "index" "name" "overallfit"

plot(cv_fit)